The rapid progress of Blockchain technology is showing no signs of slowing down. In the past few decades, many things that seemed impossible have turned out to be false, such as high transaction fees, double spending, net fraud, retrieving lost data, etc.

But, now all this can be avoided with the help of Blockchain applications. In this article, we will give you an overview of Blockchain technology and how it works in general. Let’s dive right in!

What is Blockchain Technology?

Blockchain is an append-only (unchangeable, meaning a transaction or file recorded cannot be changed), distributed digital ledger (digital record of transactions or data stored in multiple places on a computer network).

Blockchain technology increases security and speeds up the exchange of information in a way that is cost-effective and more transparent. It also dispenses with third parties whose main role was to provide a trust and certification element in transactions (such as notaries and banks).

Immutable and distributed are two fundamental blockchain properties. The immutability of the ledger means you can always trust it to be accurate. Being distributed protects the blockchain from network attacks.

Types of Blockchain Technology

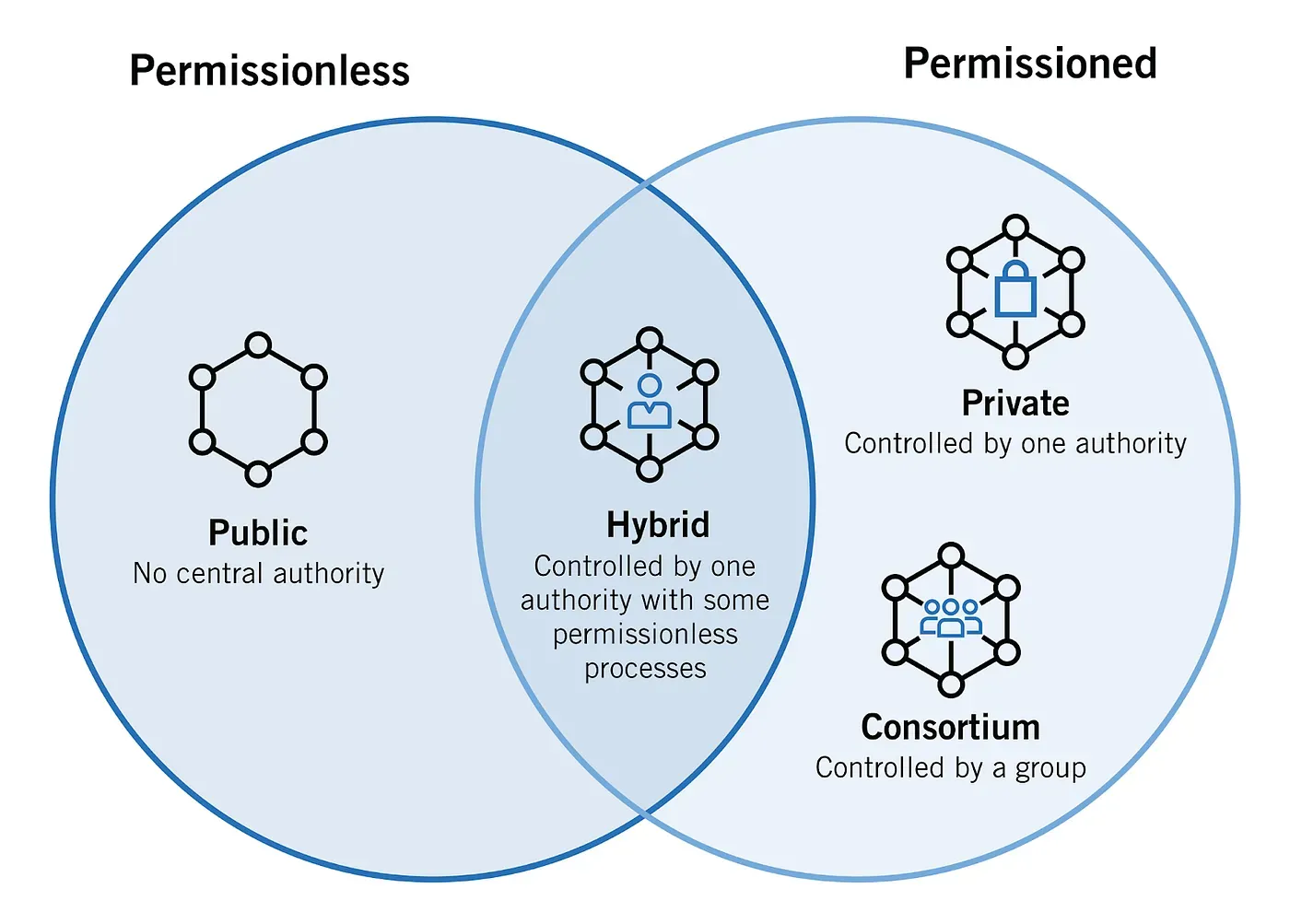

There are 2 main types of Blockchain: Permissionless blockchain & Permissioned blockchain.

(Source: Foley)

Permissionless blockchain

- Public blockchain

Public blockchains are open, allow anyone to join, and are completely decentralized. Public blockchains allow all nodes of the blockchain to have equal rights to access the blockchain, create new blocks of data, and validate blocks of data.

To date, public blockchains are primarily used for exchanging and mining cryptocurrency. You may have heard of popular public blockchains such as Bitcoin, Ethereum, and Litecoin. On these public blockchains, the nodes “mine” for cryptocurrency by creating blocks for the transactions requested on the network by solving cryptographic equations.

In return for this hard work, the miner nodes earn a small amount of cryptocurrency. The miners essentially act as new-era bank tellers that formulate a transaction and receive (or “mine”) a fee for their efforts.

Permissioned blockchain

- Private blockchain

Private blockchains are not open, they have access restrictions. People who want to join require permission from the system administrator. They are typically governed by one entity, meaning they’re centralized. Private blockchains are only partially decentralized because public access to these blockchains is restricted.

Some examples of private blockchains are the business-to-business virtual currency exchange network Ripple and Hyperledger, an umbrella project of open-source blockchain applications.

Both private and public blockchains have drawbacks — public blockchains tend to have longer validation times for new data than private blockchains, and private blockchains are more vulnerable to fraud and bad actors. To address these drawbacks, consortium and hybrid blockchains were developed.

- Consortium blockchain

A consortium blockchain is one of the different types of blockchain technology. A consortium blockchain (also known as Federated blockchains) is a creative approach to solving organizations’ needs where there is a need for both public and private blockchain features. In a consortium blockchain, some aspects of the organizations are made public, while others remain private.

It is ideal for a solution that requires collaboration across the board. For instance, supply chain, food, medicine — all of these would require collaboration across brands.

- Hybrid blockchain

Hybrid blockchain is the combination of Public blockchain and Private blockchain. They aim to combine the benefits of both of the blockchains while curbing the disadvantages of each. It has its use-cases in those enterprises that neither want to deploy a private blockchain nor public Blockchain but want to use both in order to avail the combined benefits.

With such a Blockchain network, one can have a private permission-based system and a public permission-less system as well.

Such a Blockchain network allows only a selected section of records to go public while keeping the rest confidential in the private network.

Why is Blockchain important?

Blockchain in business can reduce operational costs by removing once and for all intermediaries or business partners that may eventually be unnecessary, as it not only reduces costs and record-keeping but can also reduce the time for information exchanges — improving efficiency in communication.

While the financial sector can benefit the most from this emerging technology, other sectors that can also be truly transformed by blockchain’s potential include healthcare, insurance, transportation, real estate, retail, artificial intelligence, machine learning, and more.

Because it is a transparent and secure technology, banking, finance, and savings, may be the sectors that this technology will see widespread adoption. Digital financial services have the biggest advantage when it comes to smart contracts. The advantages come from digital assets and smart contracts. By using blockchain, banks can dramatically reduce the costs associated with bank accounts maintenance and financial transactions.

Already in more complex industries such as capital markets, financial markets, stock markets, insurance companies, sales and trade finance, Payments and domestic and international remittances will also have some business benefits including:

- Authenticity: With blockchain, financial institutions can bring data integrity and security while ensuring authenticity in their systems.

- Simplified process: blockchain can improve operational efficiency in any major sector of our society, including the ability to make a settlement, reporting, and auditing complete and transparent in real-time.

- Other blockchain capabilities: better data privacy, fewer infrastructure costs and transaction costs, compliance, security, and so on can be other potentials of this technology.

How does a Blockchain work in general?

Blockchain consists of three important concepts: blocks, nodes, and miners.

- Blocks

Every chain consists of multiple blocks and each block has three basic elements:

The data in the block.

A 32-bit whole number is called a nonce. The nonce is randomly generated when a block is created, which then generates a block header hash.

The hash is a 256-bit number wedded to the nonce. It must start with a huge number of zeroes (i.e., be extremely small).

When the first block of a chain is created, a nonce generates the cryptographic hash. The data in the block is considered signed and forever tied to the nonce and hash unless it is mined.

- Miners

Miners create new blocks on the chain through a process called mining.

In a blockchain every block has its own unique nonce and hash, but also references the hash of the previous block in the chain, so mining a block isn’t easy, especially on large chains.

Miners use special software to solve the incredibly complex math problem of finding a nonce that generates an accepted hash. Because the nonce is only 32 bits and the hash is 256, there are roughly four billion possible nonce-hash combinations that must be mined before the right one is found. When that happens miners are said to have found the “golden nonce” and their block is added to the chain.

Making a change to any block earlier in the chain requires re-mining not just the block with the change, but all of the blocks that come after. This is why it’s extremely difficult to manipulate blockchain technology. Think of it as “safety in math” since finding golden nonces requires an enormous amount of time and computing power.

When a block is successfully mined, the change is accepted by all of the nodes on the network and the miner is rewarded financially.

- Nodes

One of the most important concepts in blockchain technology is decentralization. No one computer or organization can own the chain. Instead, it is a distributed ledger via the nodes connected to the chain. Nodes can be any kind of electronic device that maintains copies of the blockchain and keeps the network functioning.

Every node has its own copy of the blockchain and the network must algorithmically approve any newly mined block for the chain to be updated, trusted, and verified. Since blockchains are transparent, every action in the ledger can be easily checked and viewed. Each participant is given a unique alphanumeric identification number that shows their transactions.

Combining public information with a system of checks and balances helps the blockchain maintain the integrity and creates trust among users. Essentially, blockchains can be thought of as the scalability of trust via technology.

History of Blockchain

Although blockchain is a new technology, it already boasts a rich and interesting history.

- 1982

The first blockchain-like protocol was proposed by cryptographer David Chaum

- 1991

Stuart Haber and W. Scott Stornetta wrote about their work on Consortiums.

- 2008

Satoshi Nakamoto, a pseudonym for a person or group, published “Bitcoin: A Peer to Peer Electronic Cash System.”

- 2009

The first successful Bitcoin (BTC) transaction occurs between computer scientist Hal Finney and the mysterious Satoshi Nakamoto.

- 2010

Florida-based programmer Laszlo Hanycez completes the first-ever purchase using Bitcoin — two Papa John’s pizzas. Hanycez transferred 10,000 BTC’s, worth about $60 at the time. Today it’s worth $80 million.

The market cap of Bitcoin officially exceeds $1 million.

- 2011

1 BTC = $1USD, giving the cryptocurrency parity with the US dollar.

Electronic Frontier Foundation, Wikileaks, and other organizations start accepting Bitcoin as donations.

- 2012

Blockchain and cryptocurrency are mentioned in popular television shows like The Good Wife, injecting blockchain into pop culture.

Bitcoin Magazine was launched by early Bitcoin developer Vitalik Buterin.

- 2013

BTC’s market cap surpassed $1 billion.

Bitcoin reached $100/BTC for the first time.

Buterin publishes “Ethereum Project” paper suggesting that blockchain has other possibilities besides Bitcoin (e.g., smart contracts).

- 2014

Gaming companies Zynga, The D Las Vegas Hotel, and Overstock.com all start accepting Bitcoin as payment.

Buterin’s Ethereum Project is crowdfunded via an Initial Coin Offering (ICO) raising over $18 million in BTC and opening up new avenues for blockchain.

R3, a group of over 200 blockchain firms, is formed to discover new ways blockchain can be implemented in technology.

PayPal announces Bitcoin integration.

- 2015

Number of merchants accepting BTC exceeds 100,000.

NASDAQ and San-Francisco blockchain company Chain team up to test the technology for trading shares in private companies.

- 2016

Tech giant IBM announces a blockchain strategy for cloud-based business solutions.

The government of Japan recognizes the legitimacy of blockchain and cryptocurrencies.

- 2017

Bitcoin reaches $1,000/BTC for the first time.

The cryptocurrency market cap reaches $150 billion.

JP Morgan CEO Jamie Dimon says he believes in blockchain as a future technology, giving the ledger system a vote of confidence from Wall Street. Bitcoin reaches its all-time high at $19,783.21/BTC.

Dubai announces its government will be blockchain-powered by 2020.

- 2018

Facebook commits to starting a blockchain group and also hints at the possibility of creating its own cryptocurrency.

IBM develops a blockchain-based banking platform with large banks like Citi and Barclays signing on.

- 2019

China’s President Ji Xinping publicly embraces blockchain as China’s central bank announces it is working on its own cryptocurrency.

Twitter & Square CEO Jack Dorsey announces that Square will be hiring blockchain engineers to work on the company’s future crypto plans.

The New York Stock Exchange (NYSE) announces the creation of Bakkt — a digital wallet company that includes crypto trading

- 2020

Bitcoin almost reaches $30,000 by the end of 2020.

PayPal announces it will allow users to buy, sell and hold cryptocurrencies.

The Bahamas becomes the world’s first country to launch its central bank digital currency, fittingly known as the “Sand Dollar”.

Blockchain becomes a key player in the fight against COVID-19, mainly for securely storing medical research data and patient information.

REFERENCES:

- Blog: What is Blockchain Technology and How Does It Work?

- Article: Blockchain Technology defined

- Article: Blockchain For Beginners: What Is Blockchain Technology? A Step-by-Step Guide by Nick Darlington

- Article: Types of Blockchain: Public, Private, or Something in Between by Kathleen E. Wegrzyn Eugenia Wang

- Article: Why Blockchain is Important? Here is Everything You Need to Know